Media kit

Media kit

A few days before its opening, Global Industrie unveils an exclusive study on subcontracting in Europe and France, carried out by Global Industrie consultant Daniel Coué.

Subcontracting in Europe

In 2017:

Total sales for the industrial subcontracting sectors in the former Europe of 15 amounted to 431.1 billion euros (an increase of 4 %).

This figure corresponds to the activities of 259,647 companies, employing 3.4 million people directly involved in subcontracting tasks (full-time equivalent). This represents an increase of 1.17 %.For the Europe of 28, the increase in value reached **4.34 % (523.4 billion euros). And the workforce grew by 1.69 % (4.8 million employees).

With very few exceptions, all European countries saw a clear return to growth in 2017. This upward trend even accelerated in the second half of the year. This explains the "good figures" recorded in most countries, notably France. Overall, industrial subcontracting grew by 4 % in the former Europe of 15 and by 5.93 % in the 13 new members of the European Union.

Nice growth, then! All the more pleasing in that it contrasts sharply with the slump of recent years... Be careful, though! The Old Continent's economy remains convalescent. The distant after-effects of the 2007-2009 crisis are still fading. Fiscal restraint measures taken by state authorities are preventing a more solid recovery and a more predictable economic situation. Although these policies are tending to ease somewhat, support for the economy is still very limited. Moreover, fiscal pressures remain high and remain lenitive, if not recessionary. Rising raw materials and energy prices are also causing concern among manufacturers. International competition is intensifying. And the gradual rise in the euro-dollar parity is likely to weigh on the export competitiveness of European companies.

For the time being, these negative phenomena are being opportunely offset by the upturn in global growth, at around 3.5 % (6 to 7 % for industrial production)... This is essentially what is driving economic performance upwards.

All in all, European subcontracting is doing quite well... and that's what we should remember!

Subcontracting in France

In 2017:

Total sales generated by French subcontracting companies reached 73.67 billion euros, up 4.76 % on 2016.

The industrial subcontracting sector includes 31,054 companies of all sizes, employing 507,224 people (full-time equivalent). This represents an increase of 1.60 %.

Last year saw a further increase in the activities of companies with 20 or more employees, confirming the recovery that began in 2015 and 2016. This growth was essentially due to a marked improvement in the international economic climate, which benefited both the direct exports of subcontractors and their indirect exports, via the foreign sales of principals. Despite a slight slowdown at the end of 2016, the trend continued in the first half of 2017. Above all, it became much more pronounced in the final months of the year. This explains why the final results are significantly higher than our previous estimates.

We must be wary of describing these figures as "euphoric". Especially as they are part of a climate that is highly unpredictable over the long to medium term. But they do mark a superb upturn after the calamities and bumps of 2008 to 2014.

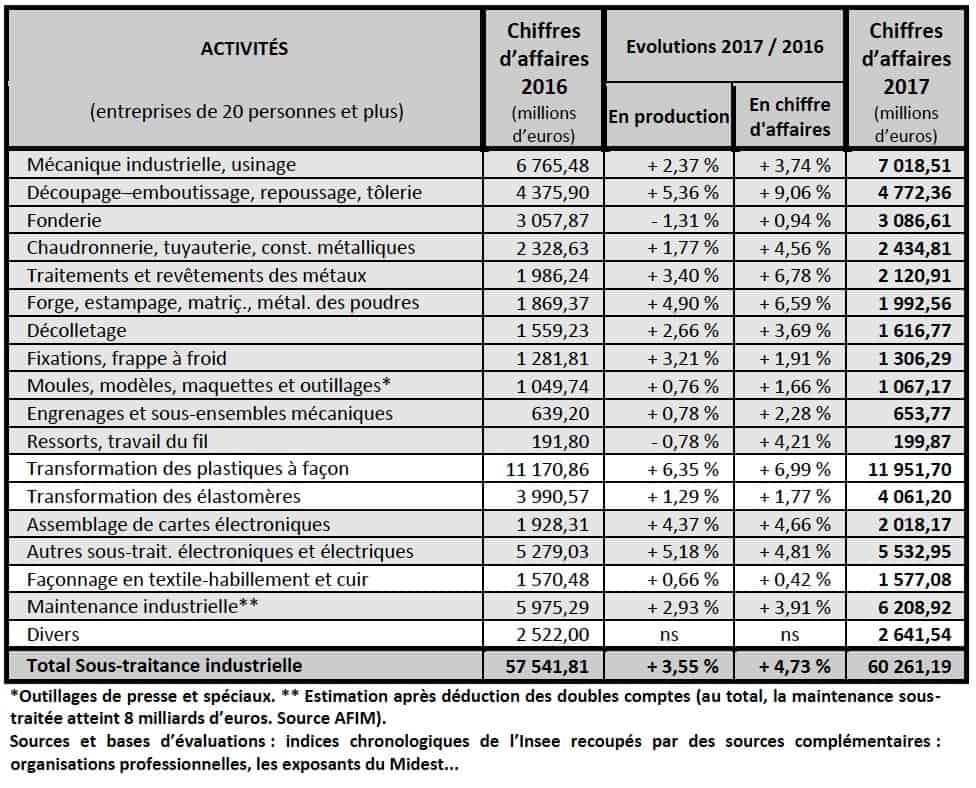

A closer look reveals sharply contrasting situations by sector. Averages don't tell the whole story! The figures need to be analyzed in detail. This is made possible by the table shown in the image above.

As can be seen, improvement has been slower in some activities than in others. But the positive signs dominate. The best scores, in terms of both production and sales, are to be found in stamping, metal treatment, forging, plastics processing and electronics and electrical engineering subcontracting. On the other hand, sectors such as molds, patterns and tooling, gears and mechanical sub-assemblies, elastomer processing and textile shaping score below the overall average.

Two sectors - casting and the manufacture of springs and wire components - are still experiencing a downturn in their production activities. But they too are returning to positive sales figures.

Prices... That's the other good news of 2017!

For industrial subcontracting as a whole, market prices rose slightly. The overall rise was 0.94 %, compared with a fall of 0.14 % in 2016. Nothing to get excited about! But still. Here too, a long trend is being reversed.

There are two main reasons for this:

- With growth, production capacities return to more satisfactory utilization rates (84 % on average), and competition tends to ease.

- The increases in raw material prices, which reappeared around a year ago, have been partly passed on in sales prices. Not all sectors and companies are on the same footing in this respect. Relationships of power with clients and negotiating skills with materials suppliers play a key role. A vast subject!

On the whole, these trends give cause for optimism. But with due caution! For, on closer inspection, the figures are mixed, confirming the uncertain nature of the current recovery. Our industry continues to be buffeted by the winds of the "globalized" economy and the whims of decision-making centers that are often exogenous. However, it is undeniably benefiting from real, sustained growth. And subcontracting is clearly benefiting. And that's the main thing...

Learn more: www.global-industrie.com