Media kit

Media kit

Symop has released its third-quarter 2016 business situation update on capital goods.

Until early 2016, French growth was underpinned by a combination of favorable factors. Corporate operating results improved, and capacity utilization in manufacturing recovered in part. GDP grew dynamically in the first quarter, before declining in the second. The origin of this uneven profile lies in particular in the suramortissement measure, which led to a very sharp acceleration in productive investment at the start of the year. Following this downturn, growth is expected to return in the third quarter, albeit at a slower pace.

In July, manufacturers continued to anticipate a clear increase in investment compared with 2015 (+6 1TP6Q), across all major industrial sectors. In its September survey, the Banque de France noted continued significant growth in investment loan applications, excluding real estate. The "suramortissement" measure seems to be playing its role in encouraging the renewal of industrial facilities.

As for industrial activity itself, after a dip over the summer months, industrial activity improved at the end of the third quarter. Manufacturers are more optimistic about their production prospects, and their order books are replenishing overall, even if foreign orders are virtually stable.

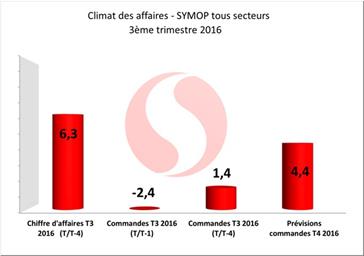

This economic climate remains favorable for capital goods suppliers. After a buoyant second quarter, sales by Symop's respondents maintained significant growth compared with the same quarter of 2015 (+6.3 1TP6Q). Contrary to previous quarters, this increase is essentially due to the domestic market, driven by the suramortissement scheme. Exports are tending to run out of steam, with sales remaining stable after the growth seen in previous quarters. Sales of special-purpose machines, such as those for packaging and wrapping, remain buoyant, particularly in the agri-food sector. 80 % of respondents report stable or rising sales on the domestic market. Fewer of them recorded an increase in export sales (75 % of exporters versus more than 80 % in the previous quarter).

The third quarter was still impacted by the closure of factories for summer vacations. Orders to capital goods suppliers were therefore slightly down on the previous quarter (-2.4%), which had recorded strong growth (+9 %). They are up by 1.4 % compared with the same quarter of 2015. Domestic demand is underpinned by the transport sectors, in particular aerospace and automotive, but also rail.

Favourable forecasts for export business were only partly realized, as the global economy remains sluggish. However, several positive signs point to an improvement in international orders towards the end of the year.

Demand for automated/robotized solutions, industrial optical and measuring equipment, and packaging machines remains strong.

The volume of order books is considered normal or above normal by more than 80 % of respondents. The increase in consultations and design work is a good sign for the coming months. 35 % of manufacturers report an increase in consultations, compared with 20 % in the previous quarter.

For the next quarter, manufacturers anticipate a 4.4 % increase in orders, both on the domestic and export markets. Due to the seasonal effect, business always picks up at the end of the year on the domestic market, with budget queues. And the tax rebate scheme should further accentuate demand. However, this forecast remains very reasonable. Is it a question of taking into account manufacturers' very relative confidence in the outlook for 2017, or of already anticipating a slowdown in investment?

Learn more: www.symop.com