Media kit

Media kit

Every quarter, Symop, the trade organization for industrial solution providers, publishes a review of the current situation for suppliers of production equipment.

According to the business leaders surveyed in April, the economic climate continued to deteriorate in the first quarter of 2020, after two quarters already in decline. However, the months of January and February had shown a slight improvement in demand, which came to an abrupt halt with the pandemic.

The January Insee survey on investment expectations predicted slight growth in investment for 2020. This was indeed the case in the first two months of the year, with demand for accessories, cutting tools and welding products all in line. The business climate has become more uncertain in view of the development of the health crisis beyond China's borders and its expected impact on international trade. In fact, orders from China, but also from the United States and European countries themselves affected by the repercussions of the health crisis, fell as early as February.

Sales for the quarter contracted by -1.4 % overall, but by -2.3 % on the domestic market. This was a slight fall, attributable to the fortnight's confinement, during which business levels fell by 60 %. Export sales fell by 3.4 %, impacted by the health crisis which prevented machine deliveries.

Order intake followed the same trends as activity in the quarter. More than half of the participants recorded an increase or stability in new orders over the quarter. A quarter saw a drop of around 5 %. Suppliers of production machinery to the French market were more affected by the slowdown. With a strong focus on export markets, manufacturers consider their order books to be at a healthy level, with several months' production scheduled to date. But 76 % of participants, suppliers in France, consider their order book to be below normal. As the survey was carried out in April, the responses undoubtedly anticipate the future repercussions of containment on customer activity and cash flow. Respondents are concerned that these repercussions will undoubtedly intensify during the summer, despite the government aid measures in place.

Suppliers anticipate a significant downturn in 2020

In this very particular context of the pandemic, which is preventing the delivery of machines due to transport or logistics problems, on-site maintenance due to company closures or access denied by customers for health reasons, and customer consultations due to a lack of hotels, business over the coming weeks will undoubtedly be severely disrupted. In an early sign, the workload of design offices and the number of consultations is already down for 58 % of respondents. And in April, suppliers recorded temporary suspensions of orders, postponements of projects under study, and even firm cancellations.

Under these conditions, forecasts can only be negative. All respondents anticipate a sharp drop in new orders in the second quarter (-13 % on the domestic market), and in the traditionally low third quarter due to the vacations. 51 % of participants expect orders to fall by more than 20 %. This will be the case for machine tools, where the drop in sales is estimated at 30 % over the year as a whole compared with 2019, with temporary contractions of up to 50 %. This trend is shared by all European countries.

Robotics activity contracted sharply (-10 %), heavily impacted by difficulties in the automotive sector. Orders also stalled, down 7 % over the quarter, with a lower-than-normal backlog as a result of a significant drop in consultations. Robotics specialists see no improvement over the coming months.

Suppliers of machine consumables, measuring equipment and welding products maintained a satisfactory level of activity over the first two months, only to suffer the effects of the pandemic. New orders remained at a satisfactory level. Manufacturers do not expect business to pick up before September.

The impact of the health crisis was brutal, but business is picking up slowly

In mid-March, when the health crisis led to a lockdown, Symop immediately set up a barometer to monitor companies' response to the looming economic crisis. Members were asked to update the barometer every two weeks.

A study of the successive sequences shows that by the end of March, the level of activity of member companies had fallen by 55 %, with the closure of services within companies. Fortunately, this level has been rising since the beginning of May among suppliers of capital goods (58 % in mid-May).

It was of course the general, administrative and financial departments that remained active throughout the crisis, with 75 % of personnel. Many production sites were closed, preventing the delivery of machinery and equipment. Only 34 % of production workshop employees maintained production in the early stages of containment, rising to 45 % by the end of April. Today, we are seeing a slow recovery, with 50 % of staff employed in manufacturing. A similar trend can be observed in the sales department, where the number of active sales staff has risen from 38 % to 60 %. Throughout this period, commercial relations were difficult to establish, due to the fact that travel was forbidden, and hotels and restaurants were not available for long trips.

Similarly, on-site after-sales and machine maintenance services were unable to operate normally. Site closures, bans on entering workshops for health reasons, and a lack of hotel facilities made travel impossible. Only 26 % of employees were working at the start of the crisis, compared with 56 % today.

To cope with this contraction in activity, 36 % of employees took advantage of short-time working measures at the start of the crisis, supplemented by requests to take leave or RTT. This use of government aid fell with the recovery, and stood at just 14 % at the end of May. It should be noted that no redundancies were prepared over the period, as manufacturers were aware of the difficulty of recruiting.

Telecommuting has been adopted by all companies: at the height of the crisis, it reached 75 % of employees. Of course, on-site presence is increasing as the industrial fabric recovers.

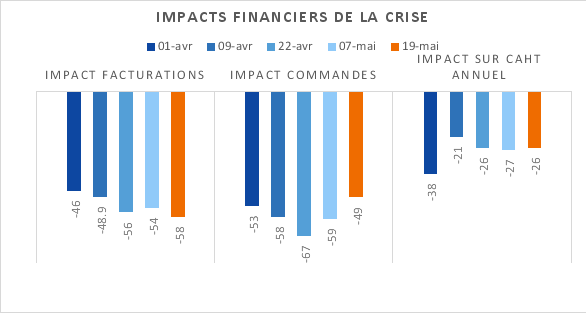

On the other hand, the impact of the crisis on demand and invoicing continues to worsen, even with the upturn in manufacturing.

Orders contracted sharply, from the usual -53 % at the beginning of April to -58 % and even -67 % at the end of April. They are still 50 % lower at the beginning of May.

The same applies to billings, which have fallen sharply from -46 % at the end of March to -58 % today, as the depletion of the order book only reduces future billings.

For the year as a whole, manufacturers are currently forecasting a 26 % drop in their budgeted sales for the year.

Visit the site:

www.symop.com